When Does a Line of Credit Stop Being Enough for a Growing Practice?

If your practice already has a line of credit, do you need anything more?

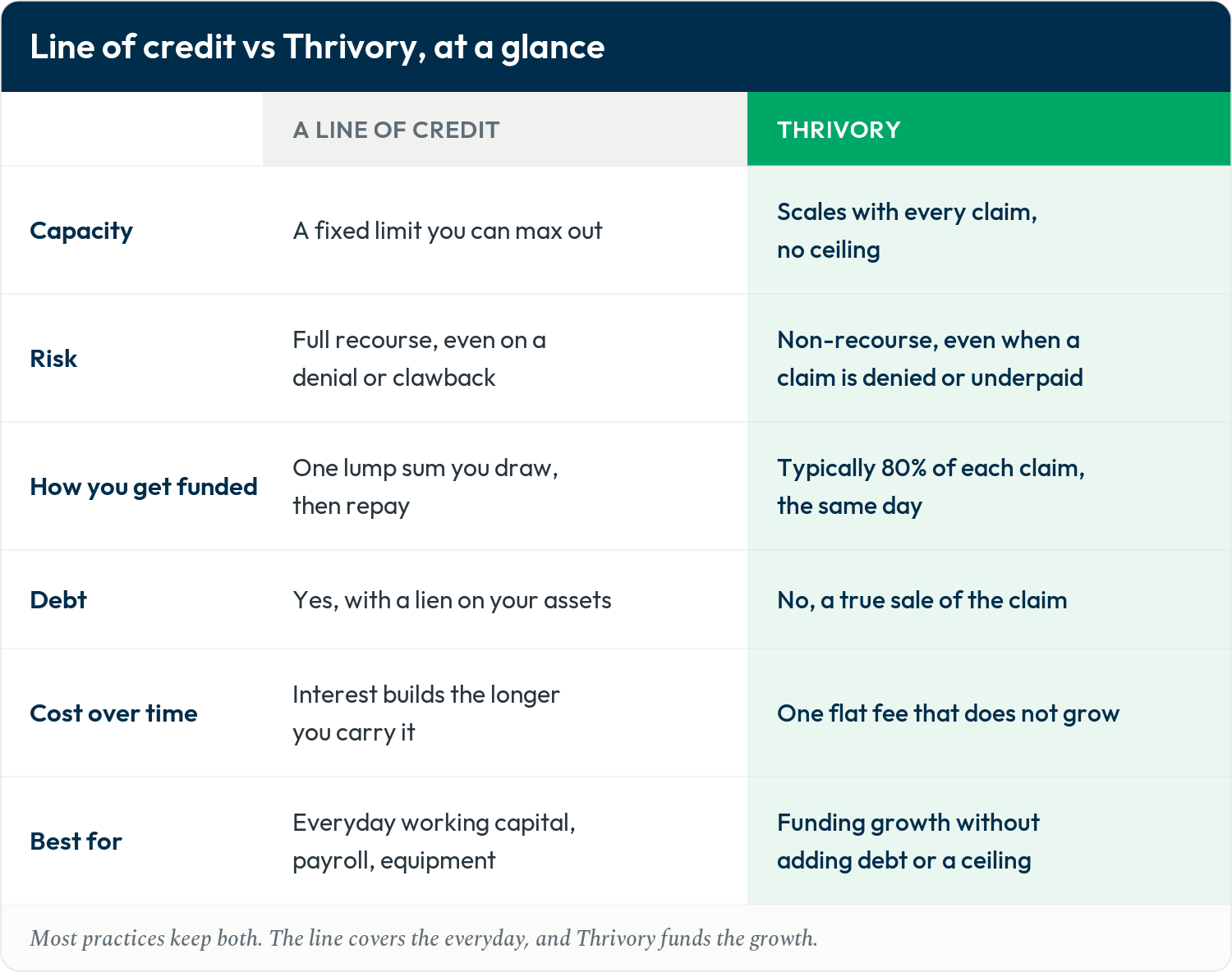

It is a fair question, and for plenty of practices the answer is no. A line of credit is a good tool. But it was built for one job and a growing practice eventually runs into the limits of that job. The trick is knowing when you have hit that point, before it starts costing you.

What a line of credit is good at

A line of credit is short-term working capital with a fixed limit. You draw what you need, pay interest on the balance, and pay it back. It handles the everyday gaps well: making payroll in a slow month, covering a surprise repair, buying a piece of equipment, or bridging the weeks before a big deposit lands. The only question is whether it can keep up with a practice that is growing fast

Where the ceiling becomes the problem

A line of credit has a fixed number on it, and that number does not move until you go back to the bank to renegotiate. For a steady practice, that is rarely an issue. For a growing one, it is a constant ceiling, because growth in healthcare is mostly volume. More patients, more visits, more claims.

This is where thin margins matter. On a slim margin, you do not grow by charging more. You grow by seeing more patients. But every new patient costs you up front, in staff, supplies, and chair time, all spent weeks before the payment shows up. If your capital is capped at a fixed limit, your patient volume is capped right along with it. You can end up turning away referrals you are fully equipped to handle, because the cash to deliver that care is locked in claims you have already filed.

How Thrivory fits

That is the gap Thrivory fills. It typically advances 80% of a claim’s expected value into your account the same week you file it. It is not a loan, so it adds no debt. The cost is a single flat fee, locked the day you are funded. A line of credit charges interest instead, and that rate floats with the Fed and grows the longer you carry a balance. The flat fee does neither. It will not climb if rates rise, and it will not grow if a claim takes a while to pay. Your billing does not change, and your payments still land where they always have. The difference that matters for a growing practice is that there is no ceiling. The funding scales as your claims do, so the more care you deliver, the more capital is available to deliver more.

Who carries the risk when a payer is slow or says no

There is also a real difference in who carries the risk. A line of credit is full recourse. You repay the bank on its schedule no matter how your reimbursements actually come in, so if payers run slow or deny a batch of claims, that shortfall is yours to cover.

Thrivory’s program is different. If Thrivory advances on a claim that was expected to pay and the payer denies it, Thrivory takes the loss. They write it off and do not come after the practice to pay it back. The carve-outs are narrow, limited to things a provider controls, like improper billing or fraud. So a denial on a claim you were funded on does not turn into money you suddenly owe.

What it means if a raise or a sale is coming

This also matters if a raise or a sale is anywhere on the horizon. A line of credit is debt, and it adds to the leverage an investor or a buyer scrutinizes in diligence. An advance on revenue you have already earned is not a loan and does not add debt. It is your own revenue, moved forward, not money borrowed against the practice.

When a line of credit is not an option

Sometimes a line of credit is not available at all. Banks attach covenants, they usually want a personal guarantee that puts your own assets behind the practice, and they often want to see two or more years in business before they will lend. Not every growing practice clears those terms, and plenty that could would rather not. Thrivory looks at something different: the claim and what it is expected to pay, not your personal assets or your time in business. For a lot of practices, that is the whole reason the conversation starts.

What that actually unlocks

The payoff is real. One practice we work with grew revenue 75%, a 5.9x return on the funding they used, by pouring the freed-up cash back into growth by hiring another provider, adding more infusion chairs, and expanding locations across the state of Michigan. All of it paid for by claims they had already earned, just sooner.

So how do you know if you are there yet?

None of this means dropping your line of credit. Most practices we work with keep theirs and use it for exactly what it does best. The shift is narrower than trading one for the other. It is the point where you stop growing by borrowing against a fixed limit and start funding growth with revenue you have already earned.

If you still have room on your line and you are not feeling the ceiling, you are not there yet, and that is fine. But if the limit is starting to feel like a limit, that is usually the sign that your practice has grown into a different kind of question.